Unless your industry was one of the few that were helped by the 2020 pandemic, your small business has likely experienced financial and other difficulties and may still struggle. With all the economic upheaval, social movement, government programs, executive orders, and administrative changes still going on, it may be difficult to estimate your company’s 2021 budget needs and expectations.

If you are new to owning rental properties, you might have many questions about your investment’s tax implications. You could file a few different tax forms, with differing purposes, depending on the actual services you supply. There are also several other considerations regarding rental tax filing and amounts due.

The end of one year and the beginning of the next should always prompt small business owners to think about their business resolutions for the coming year. This is true for 2021 more than any other recent year, after enduring what 2020 brought. These six resolutions not only apply to most small businesses for the coming year but are useful for years to come.

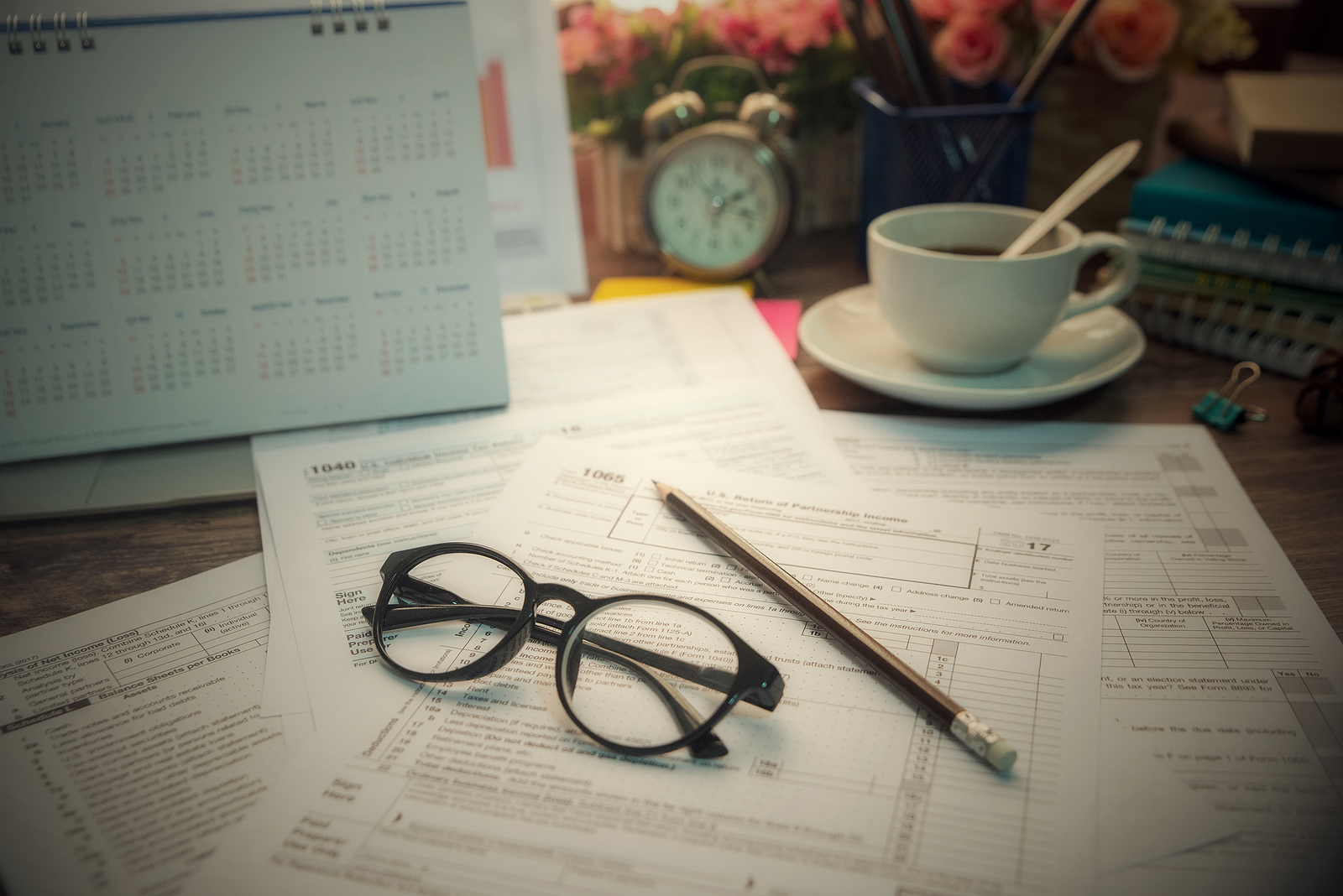

The year 2020 was a topsy-turvy year, financially, for most Americans. Some were able to continue working and earning with little or no interruption, while at the other end of the spectrum, some lost their livelihoods. Some were ineligible for unemployment and many others landed somewhere in between. Whatever your situation, this would be the year to start your tax preparation early with a virtual consultation and planning meeting.

Scams by phone or email have been around for years. With COVID-19 dominating 2020, scammers have become more creative and relentless. Between online shopping and year-end fundraising, the season will almost certainly include attempts by scammers to get your money.

Your business has undoubtedly been affected by the COVID pandemic. If it was once prosperous and viable, it can one day again be successful, even in a future which may never go back to “normal.” Pivoting is returning to a business model that existed during your startup to make possibly large or extreme adjustments to accommodate new growth or a changing external business environment. In the case of COVID-19, the business environment is almost alien, and to survive and thrive, pivoting to embrace and make changes is necessary.

The world of business has changed in ways that were unimaginable just a few months ago. The change has been coming for a long time. Still, with the recent pandemic, quick advances in the virtual office, sales, meetings, customer service, and other aspects of doing business have been thrust upon large and small companies alike throughout the globe. While this brought many technical and procedural challenges, it’s also changed the nature of business overhead costs.

What does the future hold for your small business finances? Positive cash flow is crucial for maintaining business operations and paying employees. If you don’t manage your finances appropriately, you risk cash shortages to pay your expenses when sales slow down. Fortunately, there’s a way to help you see ahead to prevent these issues and help your business grow. Here’s how you can predict a cash shortage and prevent it from affecting your business.

What is a solopreneur, and what kind of business can a solopreneur form or develop? The term “solopreneur” is often used interchangeably with "entrepreneur," "freelancer," "self-employed" or "small business owner,” perhaps since all of them will likely have to pay self-employment taxes and file 1099 forms. While any of these terms may be simultaneously valid for your business, there are distinctions between them.

For small business owners, cash flow may be a challenge during normal times. These are not normal times. The continuing COVID-19 emergency is putting at risk the survival of many small businesses. Now, more than ever is the time for all owners to engage in a new kind of planning; new ways of monitoring and projecting cash flow.